March 2026 | The Newsletter

Monthly Stats

April 2026

We ran First Look Statistics for the month of March 2026, which are available below. The spring market is

showing real signs of life, with pending units up nearly 12% on a Year Over Year (YOY) basis and total sales

climbing 5.6%. Prices remain slightly lower YOY, but the trend lines are flattening and overall dollar volume

increased more than 4%. Mortgage rates have pulled back from their late March highs and are settling in the

low to mid 6% range, which is an improvement from where we were just a few weeks ago.

Key Highlights:

Months of Inventory (MOI) in the Metro edged up to 5.8, a slight increase from last year’s 5.6 and firmly

in balanced market territory.

YOY Avg Sold Price declined only 1.3% to $575,152 while Median Sold Price declined 2.4% to

$428,786, both of which represent a flattening trend.

Total Pending/Under Contract units jumped +11.9% YOY to 3,253, the strongest demand signal we’ve

seen in months.

Total closed sales increased +5.6% and total dollar volume increased +4.3% to $1.57 billion for the

month.

Mortgage rates have eased to roughly 6.37% (30 year fixed) after spiking above 6.6% in late March.

Avg and Median Prices Continue to Flatten

Average and Median Sold Prices both declined modestly on a YOY basis, with Avg Sold Price down 1.3% and

Median Sold Price down 2.4%. While prices remain below last year’s levels, the trend line over the past several

months shows a clear flattening pattern. We are not seeing significant further declines, and the Month Over

Month trajectory heading into spring is consistent with normal seasonal appreciation. The price per square

foot numbers tell a similar story, with Avg Sold $/SF at $253 (down 3.4%) and Median $/SF at $210 (down

5.0%). Sellers who price realistically are finding buyers, and the overall picture is one of stabilization rather

than continued decline.

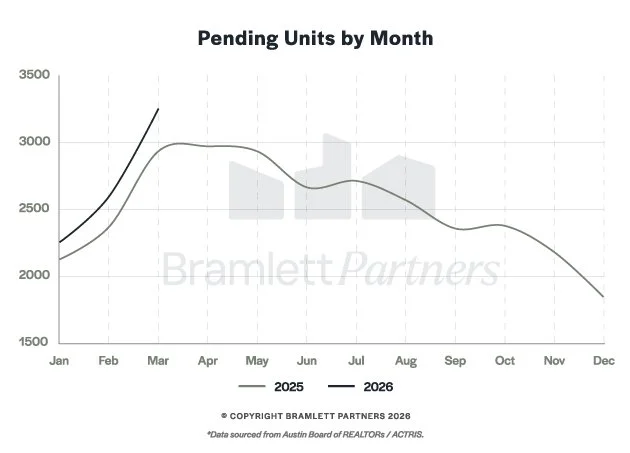

Pending Units Show Real Demand Growth

This is arguably the most encouraging data point in the March report. Pending units surged to 3,253 in March

2026, up 11.9% from 2,908 in March 2025. The 2026 pending unit curve is tracking well above the 2025

curve through the first three months of the year, which is a strong forward indicator for Q2 closings. This

increase in contract activity tells us that buyers are actively engaging and making purchasing decisions, even

with mortgage rates in the 6% range. Combined with the 5.6% increase in closed sales, the demand side of the

equation is clearly healthier than it was a year ago.

New Listings Flat While Active Inventory Grows

New listings came in essentially flat YOY at +0.5%, with 5,231 new listings hitting the market in March.

However, active inventory increased 6.5% to 16,599, which tells us that homes are sitting a bit longer before

selling (Avg Days on Market increased to 101 from 96). Withdrawn and expired listings actually declined 9.6%,

which suggests fewer sellers are giving up and pulling off the market compared to last year. The net effect is

more options for buyers and a market that rewards proper pricing and preparation.

Consumer Sentiment Drops, But Context Matters

The University of Michigan Consumer Sentiment Index fell to 47.6 in the preliminary April reading, down from

53.3 in March. This is a notable decline and the lowest reading in the survey’s history. The decline was

widespread across age, income, and political groups, largely driven by concerns around the Iran conflict and

rising energy costs. However, it’s important to note that 98% of survey responses were collected before the

April 7th ceasefire announcement, so the reading largely reflects pre‐ceasefire conditions. In recent years,

sharp drops in consumer sentiment have not always translated into reduced spending, and locally, the Austin

market’s March pending unit data suggests buyers are not yet pulling back. We will be watching this closely in

the coming months.

Mortgage Rates Ease from Late March Highs

After starting the year around 6%, mortgage rates climbed through February and into March, peaking above

6.6% in late March due to geopolitical uncertainty and inflation concerns. The 30 year fixed rate mortgage

averaged 6.37% as of April 9, 2026, down from the prior week’s 6.46%. This pullback is a welcome

development heading into the heart of the spring buying season. Industry forecasters expect rates to remain

near 6.3% through the rest of 2026, with some projecting rates dipping just under 6% by year end. Any

meaningful rate reduction would further support the demand trend we’re already seeing in the pending unit

data.

If you’re a buyer

The spring 2026 market is presenting a real opportunity. You have more inventory to choose from than at any

point in the last several years, prices remain below 2024 and 2025 levels in many areas, and mortgage rates

have eased from their recent highs. The increase in pending units tells us that other buyers recognize this

window too, so competition is picking up. If you find a home that works for you at a price that makes sense, this

is a solid time to act. You can always refinance if rates drop later, but you can’t go back in time to buy at today’s

prices.

If you’re a seller

The demand side of the market is genuinely improving, with pending units up almost 12% and closed sales up

more than 5%. That said, inventory remains elevated and buyers have options. Pricing your home correctly

from day one is still the single most important decision you will make. Homes that are priced well are moving.

Homes that are overpriced are sitting. Average Days on Market is 101 days in the Metro, which means patience

is required, but the data is moving in the right direction. Spring is your strongest season, so if you’re planning to

sell this year, now is the time to get to market.

Always remember that real estate is hyperlocal and hypersituational. If we can help you with your

home/property or if you’d like to strategize your situation, please reach out.

Link to full newsletter with graphics: https://drive.google.com/file/d/1dx9gTPbUUDKpGLeiksZFMPvr3F2CK27Y/view